Bethel’s $1.7B Breakthrough: How Chinese Brake-by-Wire Suppliers Are Rewiring the Global Auto Industry

Bethel’s $1.7B Breakthrough: How Chinese Brake-by-Wire Suppliers Are Rewiring the Global Auto Industry

What happens when a Chinese Tier 2 supplier sells 7.03 million intelligent braking units to eight of the world’s ten largest automakers in a single year? For Western investors still betting on Bosch and Continental to dominate the autonomous vehicle actuator market, the answer is sobering: Chinese brake-by-wire suppliers have officially moved from fringe players to existential threats.

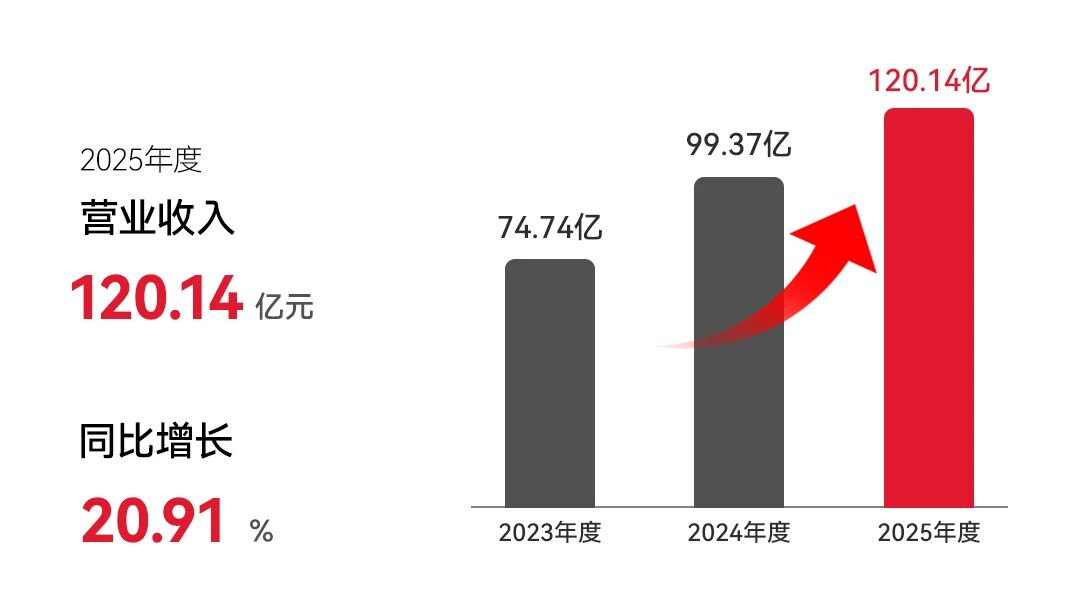

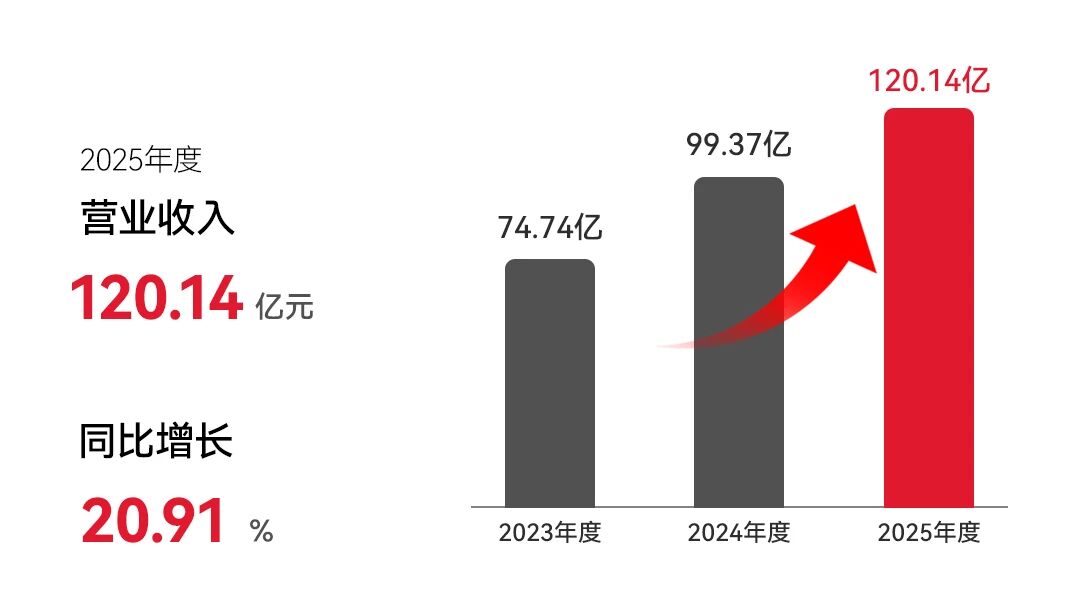

According to Bethel Automotive Safety Systems’ (603596.SH) 2025 annual report, the Wuhu-based company crossed the 120 billion yuan threshold ($1.65 billion USD), posting a 20.9% year-over-year revenue surge. But the headline figure masks a more profound shift: Bethel’s intelligent electronic control products—including the brake-by-wire systems (WCBS) critical for autonomous driving—grew 34.8% to 7.03 million units, signaling that Chinese manufacturers have solved the safety-critical engineering puzzles that once protected Western Tier 1 margins.

The End of the Western Brake Monopoly

For decades, brake-by-wire technology remained the exclusive domain of Bosch, Continental, and ZF Friedrichshafen. These German giants leveraged decades of safety systems expertise to command premium pricing on electronic braking systems—the essential actuators that translate algorithmic decisions into physical stopping power for ADAS and autonomous vehicles.

Bethel’s 2025 customer list reads like a deliberate invasion of the Western supply chain fortress. The company secured new platform contracts with Ford Europe, Renault France, and FAW-Volkswagen, adding to existing relationships with General Motors and Stellantis. With eight of the top ten global OEMs now on its roster, Bethel has achieved the scale necessary to undercut incumbent pricing by 20-30% while maintaining ISO 26262 functional safety standards.

The Mexico Manufacturing Gambit

Perhaps most alarming for Detroit executives: Bethel isn’t just exporting from China. The company’s Mexico production facility Phase 1 is already serving GM, Stellantis, and a ‘major North American EV client’ (widely speculated to be Tesla or Rivian) with brake-by-wire and EPB systems. Phase 2 expansion is underway, while a new Morocco facility—targeting 2027 production—will circumvent potential EU tariffs by manufacturing within the European sphere of influence.

This geographic arbitrage strategy, detailed in Bloomberg’s coverage of Chinese auto parts globalization, allows Bethel to offer just-in-time delivery to North American and European assembly plants while maintaining Chinese cost structures.

Why Investors Should Track the ‘571 Projects’ Metric

Bethel’s financial disclosure reveals 571 concurrent R&D projects, with 605 new designated programs expected to generate 9.5 billion yuan in annualized revenue. This pipeline diversity—spanning traditional disc brakes, lightweight components, and steer-by-wire—creates a defensive moat against Western trade retaliation.

- 318 new mass-production projects launched in 2025 alone

- 45.4% growth in new designated program value year-over-year

- German Frankfurt R&D center now operational, coordinating with Detroit facility

The Robot Pivot: From Automotive to Humanoid

Bethel’s strategic vision extends beyond vehicles. The company established two joint ventures targeting ball screw and motor production—critical components for humanoid robot joints—and invested in Chery’s humanoid robot subsidiary (墨甲机器人). With a 200 million yuan dedicated fund, Bethel is positioning its precision manufacturing expertise for the post-automotive mobility era, potentially supplying actuators for Tesla Optimus competitors.

This diversification, noted by Financial Times analysts, represents a classic Chinese industrial policy play: using automotive scale to subsidize entry into next-generation robotics, then dominating both sectors simultaneously.

Recommended Reading

For readers seeking deeper context on the geopolitical battle for automotive technology supremacy, we recommend The Powerhouse: America, China, and the Great Battery War by Steve Levine. This gripping account of the lithium-ion battery arms race provides essential historical context for understanding how Chinese suppliers like Bethel transitioned from component assemblers to technology leaders.

See our analysis on how Chinese LiDAR manufacturers are undercutting Western sensor makers for a parallel case study in autonomous vehicle supply chain disruption.

The Bottom Line for Western Markets

Bethel’s $1.7 billion revenue milestone isn’t merely a corporate achievement—it’s a market signal. As brake-by-wire systems become standard equipment for Level 3 autonomous vehicles, Western OEMs face an uncomfortable choice: pay premium prices to incumbent German suppliers, or embrace Chinese alternatives that offer equivalent safety ratings at commodity pricing.

For investors in legacy automotive suppliers, the question is no longer whether Chinese competition will arrive, but whether Western Tier 1s can maintain their 40% gross margins when Chinese brake-by-wire suppliers have already proven they can deliver at scale.