Minieye IPO Analysis: Dual-Wheel Strategy Drives Revenue Growth Amid 113% R&D Surge

Minieye IPO Analysis: Can This Tier-2 Supplier Survive the L4 Transition?

What happens when an automotive supplier burns through ¥333 million in R&D—equivalent to 44% of total revenue—to pivot toward driverless logistics? Minieye IPO analysis of the company’s first post-listing annual report reveals a business hitting record sales while hemorrhaging cash, offering a stark case study in China’s autonomous driving commercialization race.

The Financial Paradox: Revenue Up, Losses Wider

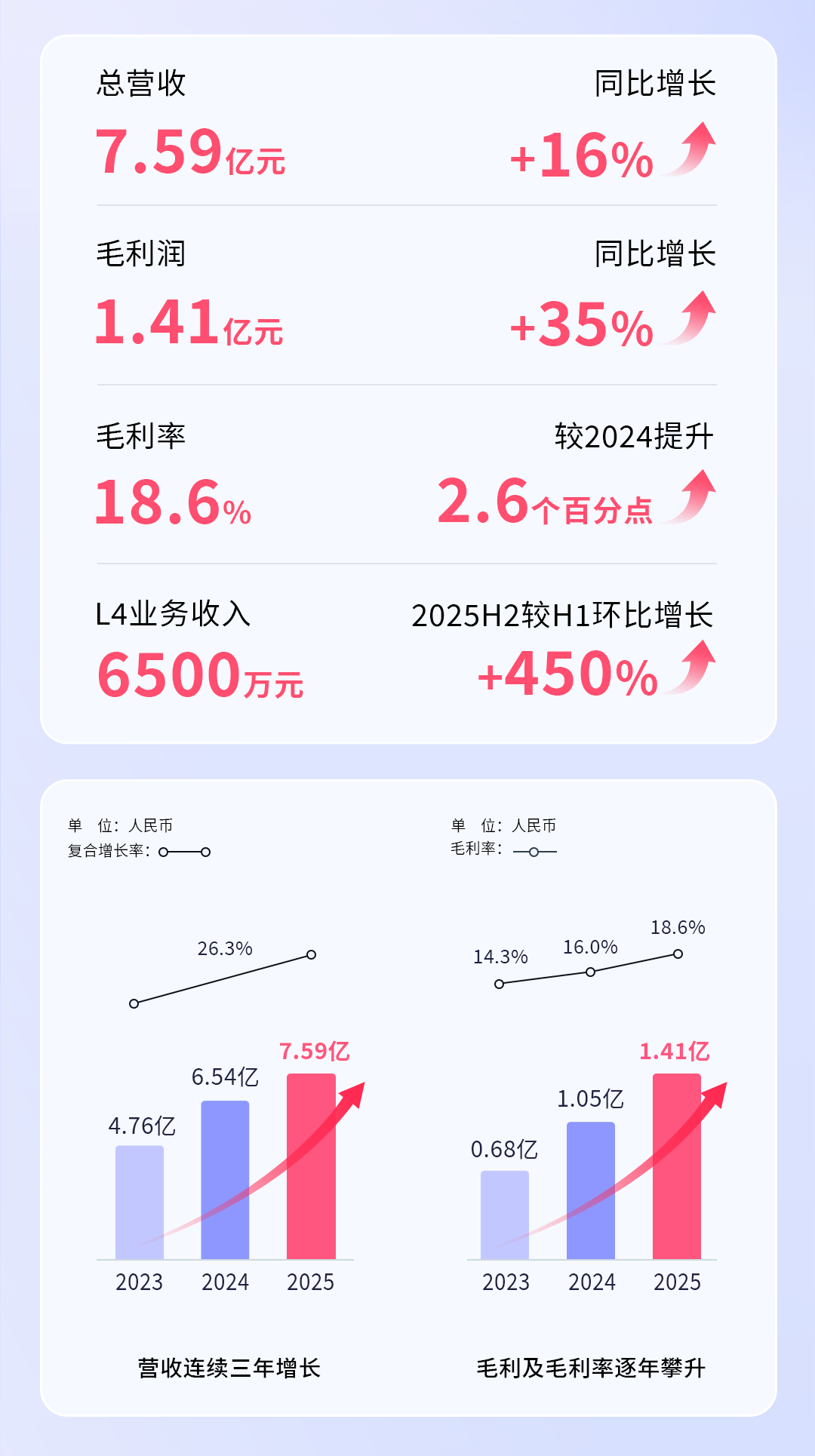

Minieye Technology (2431.HK) listed on the Hong Kong Stock Exchange in late 2024, and its fiscal 2025 results—released March 31, 2026—paint a picture of aggressive transformation. Revenue climbed 16% to ¥759 million ($104 million USD), with gross margins expanding from 16.0% to 18.6%. Yet the company posted a comprehensive loss of ¥417 million as research expenditures more than doubled, up 113% to ¥333 million.

This divergence between top-line growth and bottom-line deterioration defines the Minieye IPO analysis narrative. The company is deliberately sacrificing profitability to fund what management calls a ‘dual-wheel’ strategy: maintaining its legacy ADAS component business while building an L4 autonomous logistics operation from scratch.

Wheel One: ADAS as the Cash Cow

Approximately 85.5% of revenue (¥649 million) still derives from ‘Intelligent Components and Solutions,’ encompassing smart cockpits and driver assistance systems. This segment benefits from a regulatory tailwind: China’s pending mandate for Driver Monitoring Systems (DMS), expected implementation by 2027, with current market penetration at just 24.6%.

Strategic wins in 2025 included a platform-level project with a global automaker’s Chinese joint venture—Minieye’s first major international OEM breakthrough—and a ¥1.3 billion lifecycle contract with a state-owned enterprise. The higher-tier iPilot 4 ADAS solution grew 39% to ¥120 million, suggesting the company is successfully migrating upmarket from basic tier-2 supplier status. See our analysis on China’s Automotive Semiconductor Supply Chain for related investment risks.

Wheel Two: The L4 Logistics Gamble

Where Minieye diverges from competitors like Horizon Robotics or Hesai is its asset-heavy pivot into operations. The ‘Xiaozhu’ unmanned logistics vehicle generated ¥65 million in its first commercial year, with over 6,000 units deployed across 18 cities covering parcel delivery, cold chain, and airport logistics.

Unlike software licensing models, this business requires vehicle ownership, maintenance networks, and operational staffing—explaining the crushing R&D and capital expenditures. Minieye also secured high-profile autonomous shuttle contracts for the World Internet Conference in Tongxiang and Ezhou Airport, projects demanding safety standards far exceeding highway ADAS requirements.

Western Investor Perspective: What Minieye Signals About China AV

For US and European portfolio managers, Minieye IPO analysis offers three critical insights into the Chinese autonomous vehicle ecosystem:

- Consolidation Pressure: With R&D consuming 44% of revenue, independent tier-2s face existential funding gaps unless they achieve platform-scale OEM integration.

- L4 Monetization Reality: The ¥65 million logistics revenue proves closed-scene autonomy is commercially viable today, even as robotaxi services remain elusive.

- Regulatory Arbitrage: China’s 2027 DMS mandate creates a predictable demand window that Western suppliers must navigate through joint ventures or risk permanent exclusion.

The Verdict: Technology Transition or Cash Incinerator?

Minieye stands at an inflection point common to Chinese AI hardware startups: the transition from technology development to scalable operations. The margin improvement in core ADAS suggests operational discipline, but the L4 logistics expansion requires sustained capital that public markets may not tolerate indefinitely.

For investors, the bet is whether Minieye can achieve logistics operational profitability before the current cash runway expires—a timeline likely measured in quarters, not years.

Recommended Reading

To understand the AI strategy driving China’s autonomous vehicle ambitions, read AI Superpowers: China, Silicon Valley, and the New World Order by Kai-Fu Lee. The book provides essential context on how Chinese firms like Minieye are approaching machine learning commercialization differently than their Western counterparts. Available via Amazon.