LFP Batteries Dominate Chinese EV Market in April 2026

LFP Batteries Dominate Chinese EV Market in April 2026

Is the dominance of LFP batteries in the Chinese EV market a sign of a new era in battery technology? The latest data from the China Automotive Battery Industry Innovation Alliance (CABIIA) reveals a significant shift in the landscape of the Chinese EV battery market. In April 2026, LFP (Lithium Iron Phosphate) batteries accounted for 81.5% of the total battery installations, solidifying their position as the preferred choice for most EV manufacturers.

Market Overview and Trends

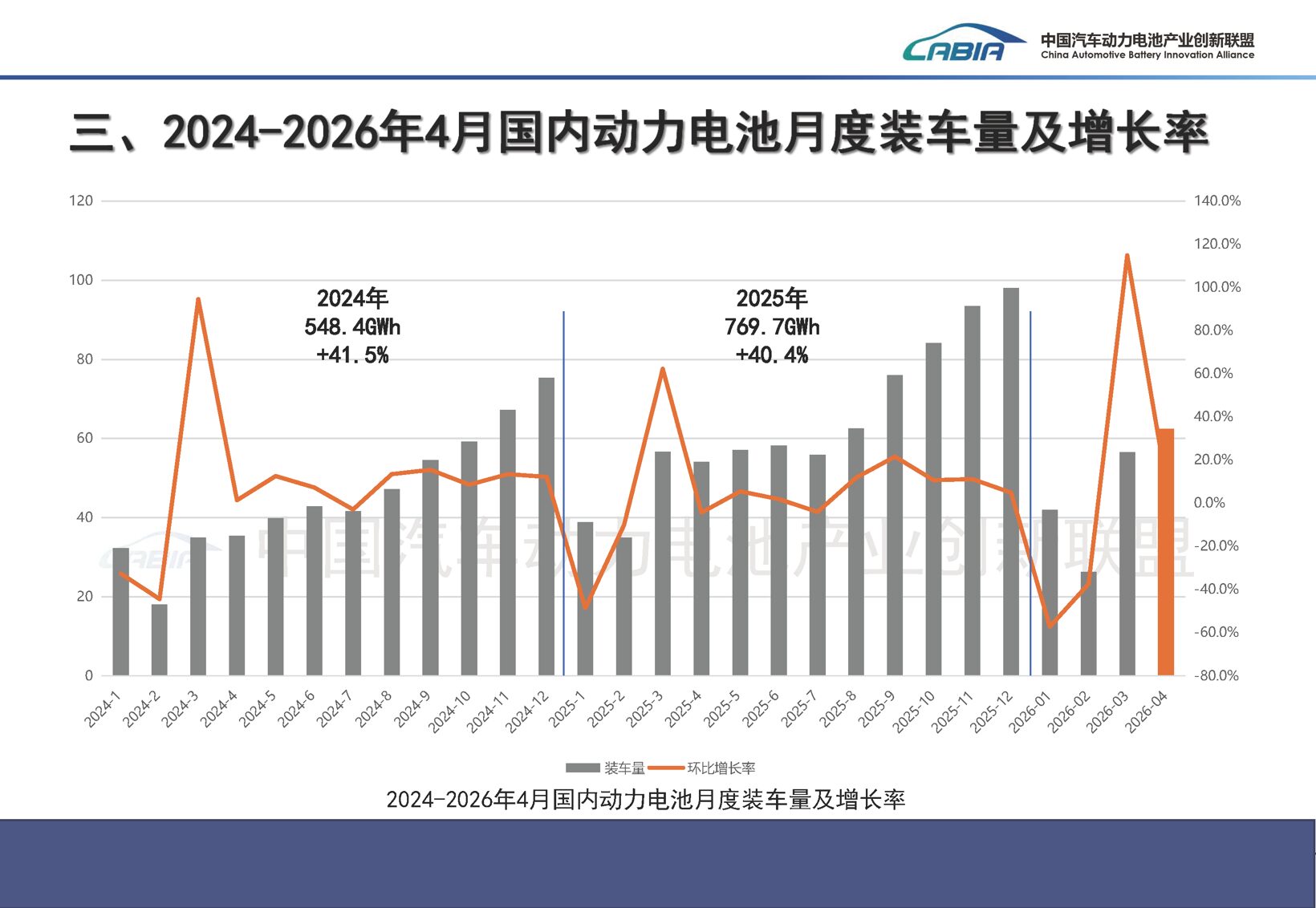

The Chinese EV battery market is undergoing a transformation, moving from capacity expansion and price wars to a focus on technological innovation, cost control, and global expansion. According to CABIIA, the total battery installations in April reached 62.4 GWh, up 10.4% month-over-month and 15.2% year-over-year. This growth reflects the robust recovery of the downstream new energy vehicle (NEV) market.

Structural Changes in the Market

Despite the overall growth, the market is experiencing structural changes. LFP batteries, with their cost and safety advantages, are becoming the dominant technology. In April, LFP batteries accounted for 50.8 GWh, or 81.5% of the total installations, surpassing the 11.5 GWh (18.5%) of NCM (Nickel Cobalt Manganese) batteries. The LFP market share has been steadily increasing, driven by the growing demand for cost-effective and safe battery solutions.

Long-Term Trends and Implications

The trend towards LFP dominance is clear. From January to April 2026, LFP batteries accounted for 149.8 GWh, maintaining an 80% market share. Although the cumulative year-over-year growth rate slightly decreased by 0.1%, this is largely due to high base figures from the previous year and some inventory adjustments by automakers. The long-term trend of LFP penetration in passenger cars, commercial vehicles, and energy storage remains strong.

Technological Advancements and Market Dynamics

While LFP batteries dominate the mass-market segment, NCM batteries still hold a niche in high-end, long-range, and export models. NCM batteries saw a 8.9% year-over-year growth in the first four months of 2026, reaching 37.4 GWh. This coexistence of LFP and NCM technologies reflects the market’s prioritization of cost-effectiveness and basic safety.

Innovations in LFP Technology

Technological innovations such as blade batteries, CTP (Cell-to-Pack) technology, and Kirin batteries are addressing the energy density limitations of LFP batteries. These advancements have enabled LFP systems to achieve stable energy densities of over 160 Wh/kg, further reducing the gap with NCM batteries.

Global Context and Investor Insights

For Western investors, the dominance of LFP batteries in the Chinese market is a critical signal. As the NEV penetration rate exceeds 40%, the consumer base is shifting from early adopters to practical users who prioritize cost, safety, and longevity. This shift is driving the adoption of LFP batteries, which offer a compelling value proposition in these areas.

Comparative Analysis

Recent articles from Reuters and Bloomberg confirm the growing preference for LFP batteries globally. For instance, Tesla’s decision to use LFP batteries in its Model 3 and Model Y vehicles underscores the technology’s reliability and cost-effectiveness. Similarly, Volkswagen and Ford are also exploring LFP options for their upcoming EV models.

Conclusion

The dominance of LFP batteries in the Chinese EV market is a clear indication of the technology’s maturity and market acceptance. As the industry continues to innovate, LFP batteries are likely to play a pivotal role in shaping the future of the global EV market. For more insights on the Chinese EV market, see our analysis on EV Battery Technology Trends.