SWIR Sensors Autonomous Driving: Korean Breakthrough Threatens LiDAR Dominance

SWIR Sensors Autonomous Driving: The Korean Breakthrough That Threatens LiDAR Dominance

What if the $50 billion autonomous vehicle sensor market is built on the wrong technology? While Western automakers bet billions on LiDAR and visible-spectrum cameras, a Korean research consortium has demonstrated a CMOS-compatible Short-Wave Infrared (SWIR) sensor that penetrates fog at a fraction of traditional costs—potentially rendering current sensor stacks obsolete before they reach mass scale.

The implications for SWIR sensors autonomous driving adoption are profound. According to Reuters automotive analysis, fog and adverse weather remain the primary technical barriers to Level 4 autonomy, causing current vision systems to degrade catastrophically when moisture obscures visible wavelengths. Now, research published in Advanced Materials by teams from DGIST, KIST, and the Korea Institute of Materials Science offers a pathway to solve this limitation while disrupting the economics of automotive perception.

The Fog Blindness Problem: Why Current ADAS Fail

Modern autonomous stacks rely on sensor fusion between visible cameras, LiDAR, and radar. Yet as noted in Bloomberg’s coverage of autonomous vehicle testing, even advanced LiDAR systems suffer attenuation in heavy fog, while cameras become functionally blind. This creates dangerous ‘autonomy gaps’ where vehicles hand control back to human drivers precisely when visibility is poorest.

SWIR technology operates in the 900-1700nm wavelength range, penetrating atmospheric obscurants that blind standard sensors. Historically, adoption has been limited by Indium Gallium Arsenide (InGaAs) semiconductor costs—often exceeding $10,000 per unit—restricting deployment to military and industrial applications. [Internal Link: See our analysis on sensor fusion limitations in Level 3 ADAS systems]

The Korean Innovation: Quantum Dots Meet 2D Materials

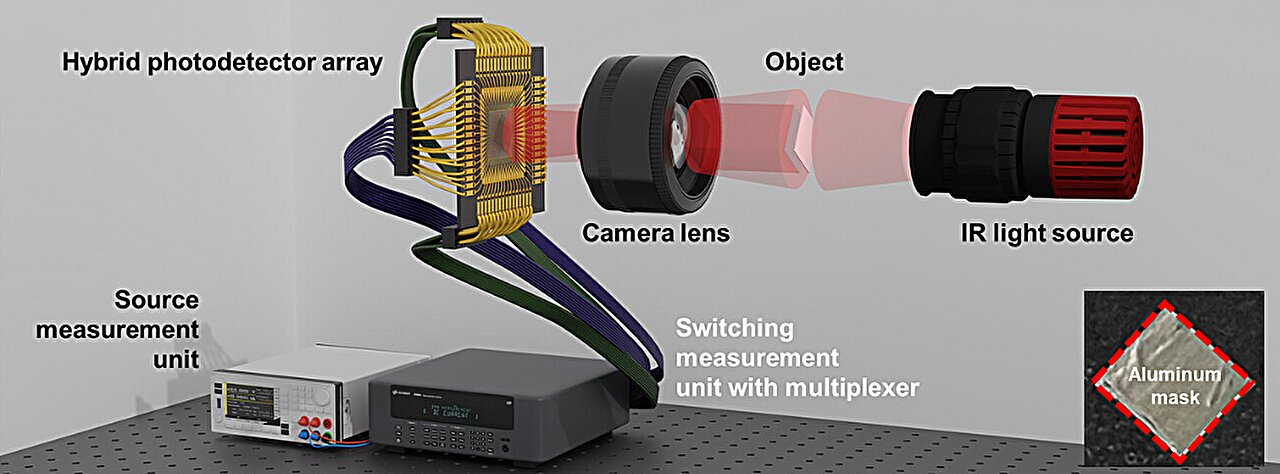

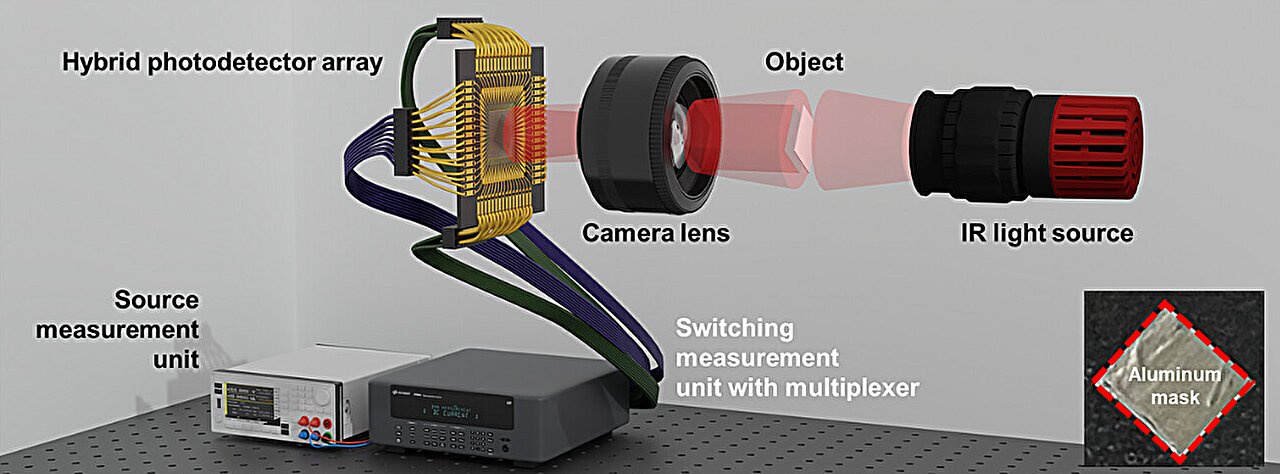

Led by Professor Jong-Soo Lee at DGIST, the Korean team developed a hybrid photodetector architecture combining silver telluride (Ag₂Te) quantum dots with molybdenum disulfide (MoS₂) 2D semiconductors. This material pairing solves the fundamental trade-off in infrared sensing: quantum dots provide exceptional light absorption but suffer slow charge transport, while MoS₂ enables ultra-fast carrier mobility that compensates for this limitation.

Performance Metrics That Rival Military Grade

The prototype demonstrated specifications comparable to expensive InGaAs sensors:

- Responsivity: 7.5×10⁵ A/W

- Detectivity: 10⁹ Jones

- Successful fabrication of 32×32 pixel imaging arrays

The CMOS Manufacturing Breakthrough

Unlike InGaAs, which requires exotic III-V semiconductor fabrication incompatible with silicon foundries, this Ag₂Te/MoS₂ process integrates directly with existing automotive CMOS production lines. As reported in Nature’s materials science coverage, this compatibility potentially reduces unit costs from thousands to hundreds of dollars—transforming SWIR from military luxury to automotive commodity and threatening the cost structures of Chinese LiDAR leaders like Hesai and RoboSense.

Investment Implications: Disrupting the Sensor Hierarchy

For Western investors tracking the autonomous supply chain, this development signals disruption across multiple tiers:

Threat to LiDAR Economics

Companies like Luminar, Velodyne, and Innoviz have justified premium pricing ($500-$1,000 per unit) through ‘fog penetration’ claims. However, solid-state SWIR cameras offer similar atmospheric penetration with no moving parts, lower power consumption, and potentially sub-$100 manufacturing costs at scale. If Korean manufacturers commercialize by 2026-2027, the economic case for automotive LiDAR weakens substantially.

Challenge to Western Tier 1 Suppliers

Traditional automotive suppliers (Bosch, Continental, Aptiv) have optimized around visible-spectrum and radar architectures. The emergence of low-cost SWIR threatens to commoditize their ADAS sensor portfolios unless they rapidly pivot to hybrid infrared-visible fusion systems.

Commercialization Roadblocks

Despite promising laboratory results, three hurdles remain before SWIR sensors autonomous driving technology reaches production vehicles:

- Resolution Scaling: Current 32×32 arrays must reach automotive-grade megapixel densities (1MP+) to compete with current camera systems

- Tellurium Supply Chain: Ag₂Te requires tellurium, a rare element currently dominated by Chinese mineral processing capacity—creating potential geopolitical supply risks

- Automotive Validation: Quantum dot stability over 15-year vehicle lifespans and extreme temperature ranges (-40°C to 85°C) remains unproven

Strategic Outlook for Western Markets

This breakthrough exemplifies Asia’s growing dominance in foundational automotive sensor hardware IP. While Western firms focus on AI software and integration, Korean and Chinese laboratories are capturing the materials science underlying next-generation perception systems.

For automakers preparing 2026-2028 model year architectures, the strategic imperative is clear: SWIR integration is transitioning from ‘nice-to-have’ to competitive necessity. Those who delay risk launching vehicles with obsolete sensor suites precisely as the industry approaches true Level 4 autonomy, while investors should monitor Korean semiconductor startups for acquisition targets before this technology scales.

Source: Advanced Materials (2024); DGIST Energy Science and Engineering; Korea Institute of Science and Technology (KIST); Korea Institute of Materials Science