Ganfeng Lithium Profit Surge: 690% Rally Signals Battery Cost Inflation for Western EV Makers

Ganfeng Lithium Profit Surge: The 690% Rally Reshaping Global EV Economics

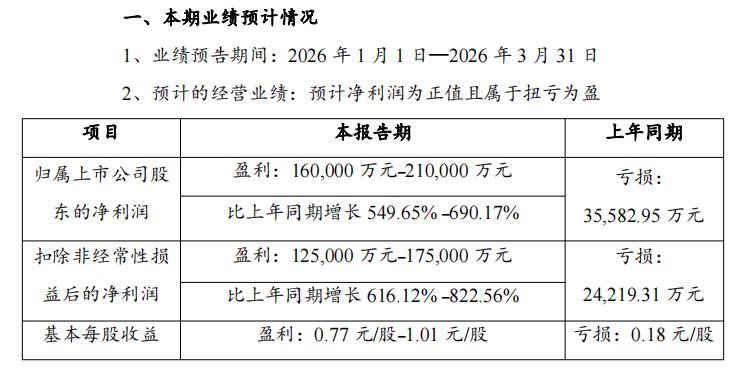

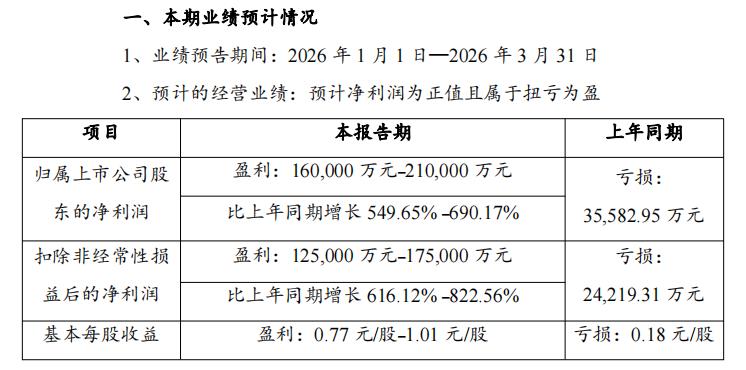

What if the era of cheap EV batteries just ended with a single earnings report? Ganfeng Lithium, the world’s largest lithium producer by market capitalization, has forecast a staggering 549% to 690% profit surge in Q1 2026—a figure that signals more than corporate success. For Western investors and automakers, this Ganfeng Lithium profit surge represents a critical inflection point: the bottom of the lithium price crash has passed, and battery cost inflation is back on the horizon.

The Shenzhen-based giant expects net profits between 1.6 billion and 2.1 billion yuan ($220-290 million USD) for the first quarter, driven by a dramatic rebound in lithium carbonate prices that has seen battery-grade material climb from roughly 70,000-80,000 yuan per ton in Q1 2025 to approximately 150,000 yuan ($20,700) per ton today. This doubling of input costs threatens to squeeze margins across the global EV supply chain just as Western manufacturers are scaling production.

Why This Matters: From Mining Profits to Your Dashboard

Western audiences typically view Chinese EV news through the lens of finished vehicles—BYD, NIO, and Xiaomi dominating headlines. But Ganfeng’s results provide a behind-the-scenes look at the commodity cycle that dictates whether Tesla, Ford, and Volkswagen can maintain their aggressive EV pricing strategies.

The Lithium Price Math Western Investors Can’t Ignore

- Price Velocity: Battery-grade lithium carbonate has stabilized around 150,000 yuan/ton after breaking through multiple resistance levels from a 120,000 yuan baseline in early Q1.

- Year-over-Year Compression: Current prices represent roughly a 100% increase from the 70,000-80,000 yuan range that plagued miners during Q1 2025’s supply glut.

- Margin Recovery: Ganfeng’s projected 16-21 billion yuan net profit marks a dramatic reversal from the industry’s brutal 2024 consolidation period.

According to Reuters commodity analysts, this rebound reflects tightening global supply chains and resurgent demand from China’s EV sector, which continues to outpace Western adoption rates by a factor of three to one.

Vertical Integration: Ganfeng’s Defense Against Volatility

Beyond raw material extraction, Ganfeng’s profitability stems from strategic vertical integration. The company reported significant volume increases in its power battery and energy storage divisions—segments that insulate it from pure commodity plays. As Chairman Li Liangbin noted, projects across Australia, Argentina, Mali, and Sierra Leone are ramping up capacity, gradually lifting resource self-sufficiency rates and optimizing cost structures.

This global asset footprint distinguishes Ganfeng from Western competitors like Albemarle and SQM, who face escalating regulatory hurdles in Chile and Nevada while Chinese firms secure offtake agreements across Africa and South America.

The 2026 Supply Crunch Warning

Perhaps most alarming for Western OEMs is Ganfeng’s executive guidance regarding 2026 market dynamics. Company leadership has signaled that lithium supply and demand will enter a ‘tight balance’ this year, with any geopolitical disruptions—policy shifts, environmental restrictions, or regional conflicts—potentially triggering severe shortages.

This contrasts sharply with the oversupply narrative that dominated 2024 analyst reports. Bloomberg Intelligence recently revised its lithium price forecasts upward, citing Chinese EV penetration rates exceeding 50% and energy storage deployment accelerating faster than mine development permits in the West.

Investment Implications: Portfolio Strategy Adjustments

For Western institutional investors, Ganfeng’s 259 million yuan ($36 million) fair-value gain from its PLS Group Ltd. investment highlights a secondary thesis: Chinese lithium giants are becoming diversified mining investment vehicles, not just commodity producers. This financial engineering—hedging collar strategies on equity positions—provides stability unavailable to pure-play Western miners.

The critical question facing US and European portfolios: See our analysis on how CATL’s pricing strategy affects Western EV makers and whether battery cost inflation will trigger a new round of EV price wars.

Conclusion: The Supercycle Isn’t Over

The Ganfeng Lithium profit surge isn’t an anomaly—it’s the canary in the coal mine for global battery economics. As lithium carbonate prices hold firm at 150,000 yuan per ton, Western automakers must confront a uncomfortable reality: the cost advantage that fueled 2024’s EV price cuts is evaporating. For investors, this signals a rotation from speculative EV startups toward established miners with proven extraction economics and Chinese market access. The lithium supercycle hasn’t ended; it has simply entered its next, more expensive phase.